Inside some of the world’s biggest asset managers, the quants are transforming a centuries-old theory to answer a burning question: What is the dollar’s true value?

At the heart of the theory is fair value, the level a currency should eventually drift toward, regardless of how expensive or cheap it is at any given point. Scholars from 16th-century Spain first measured it by price levels, proposing that exchange rates should adjust to the cost of goods so that a bag of sugar or a yard of fabric would cost the same in different nations when expressed in the same unit.

Nowadays, analysts at UBS Wealth Management and Goldman Sachs Asset Management, which oversee more than $3 trillion combined, are deploying quantitative analysis to upgrade this basic concept. The methods may vary, but they’re sending a consistent signal that should worry dollar bulls -- the greenback is too expensive after a 30 percent rally that’s lasted almost three years.

At UBS, "our models are giving exactly the same signals -- the dollar is currently strongly overvalued," said Thomas Flury, head of foreign-exchange research in Zurich. "The analyst community is too positive" on the dollar.

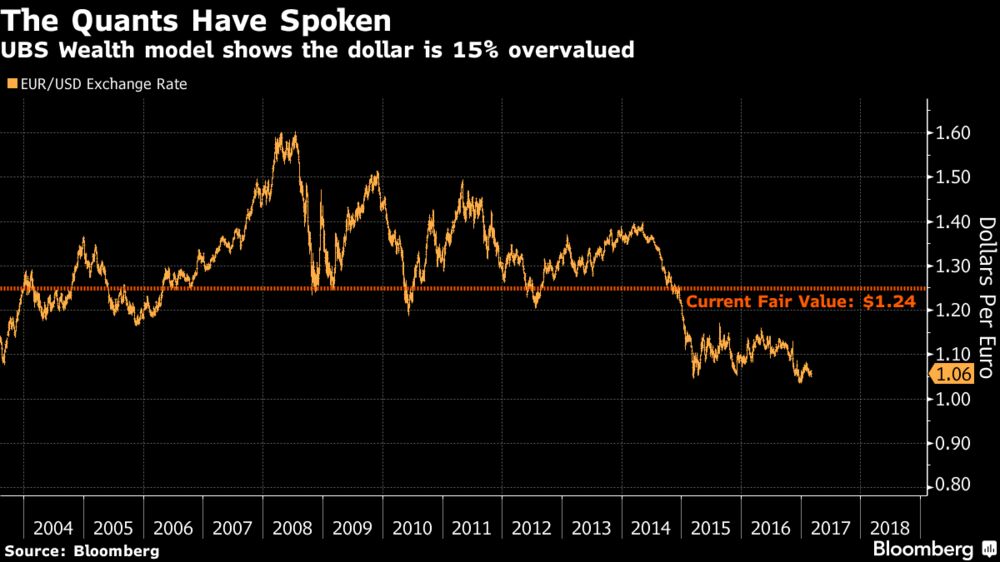

The greenback is near a 14-year high, catching the eye of President Donald Trump, who’s accused countries including Germany and Japan of keeping their currencies weak to gain a trade advantage. The dollar is about 15 percent stronger than UBS’s fair value of $1.24 per euro, and Goldman Sachs’s framework paints a similar picture. The consensus on Wall Street is that the dollar will strengthen to $1.05 against the common currency this year, from about $1.06 Tuesday, according to the median estimate in a Bloomberg survey.

UBS has two approaches. For one, it uses three decades of producer-price data to track the greenback’s deviation from equilibrium. Its analysts also have another take: They’ve developed a model that measures the share of dollar-denominated stocks and bonds worldwide over the past 20 years and assumes investors adjust allocations toward the long-term average, with the dollar being sold or bought in the process.

Terms of Trade

Over at Goldman Sachs, quantitative strategist Stephan Kessler prefers to measure the dollar through the prism of productivity. His model factors in the price of a nation’s exports over its imports. It reckons the higher the so-called terms of trade, the more competitive a country is and the higher the currency’s fair value should be.

Fair value may prove to be a dominant driver for euro-dollar at a time when the the market is debating the timing of the European Central Bank’s exit from quantitative easing, which has limited the euro’s rise. In 2013, the Federal Reserve’s announcement that it would taper its bond buying effectively removed an artificial lid and propelled the currency toward, and subsequently over, its fair value.

"Fair value matters more as we’re more toward the extremes," said Robert Davis, a portfolio manager at Putnam Investments LLC. "With any changes in the divergence theme, you’re bound to see a reversion toward fair value."

To Goldman Sachs’s Kessler, Trump’s trade rhetoric is another reason why currencies risk reverting to their underlying value this year. Both Germany and Japan run significant trade surpluses with the U.S., according to the Treasury Department, and their currencies are around 13 percent undervalued in Goldman Sachs’s terms-of-trade model.

"From a valuation perspective, most currencies should have the potential to appreciate versus the U.S. dollar," Kessler said. "This might be particularly true for countries with large trade surpluses versus the U.S. and a deep integration in the U.S. supply chain."