Last July and August, I did a 6-part series called the “Dean’s List” which looked at North American explorers and miners that could benefit from government commitments to critical minerals, like the Inflation Reduction Act. This is especially important given how many of those materials are controlled, either through mining, ownership, or processing by China, which isn’t exactly “singing from the same hymn book” as the United States and many of its allies these days. Despite the current global tensions, it also comes down to math. There just isn’t enough of many of these commodities at present to meet the explosive growth being projected in the various segments of the “green” revolution.

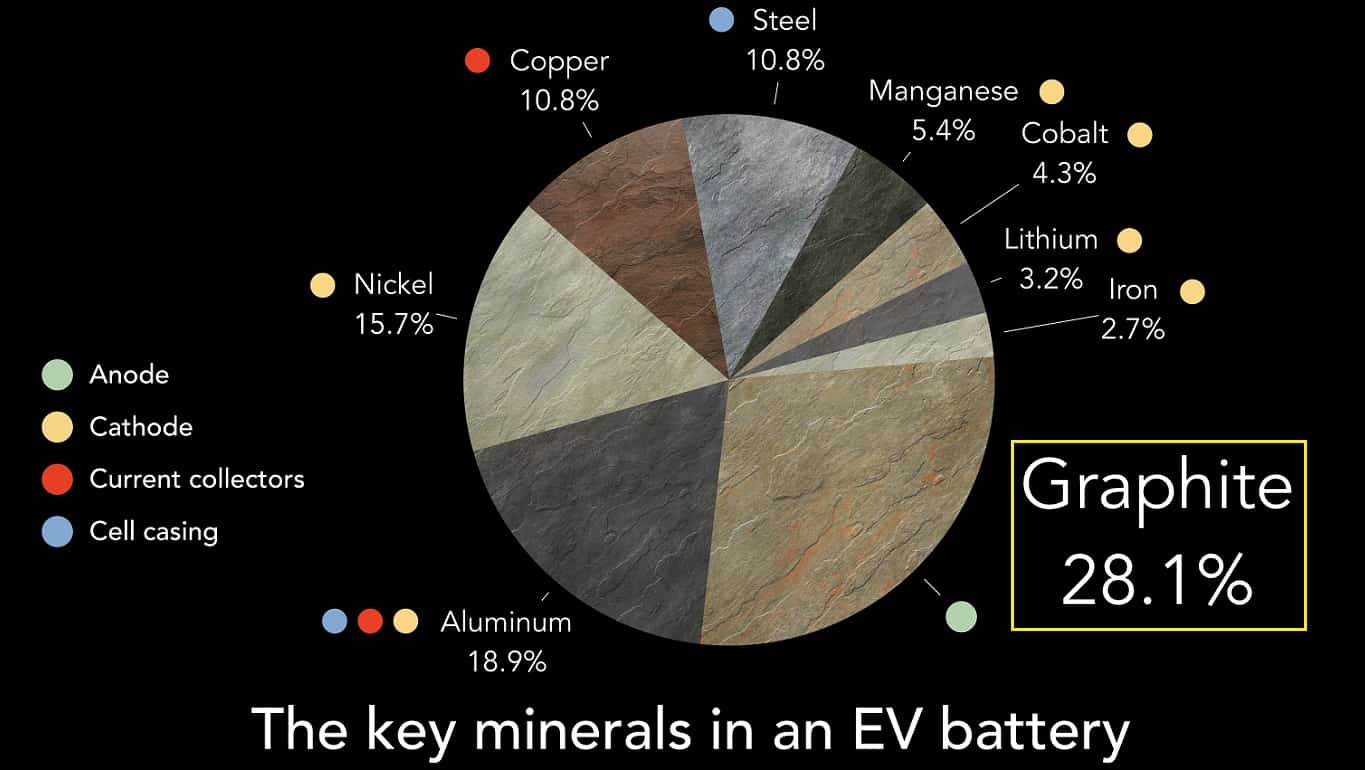

One of the articles from last year’s series focused on graphite. I consider graphite to be one of the least publicized critical minerals, especially given this anode material is the single largest component (by weight) of lithium-ion batteries used in EVs (up to 48%) and energy storage technologies. On top of that, almost 80% of graphite mine production in 2021 came from China, while China makes almost 100% of the graphite anode material. Lastly, graphite also requires the largest production increase of any battery mineral in order to meet forecast demand.

Graphite Growth Requirements for Battery Demand Forecasts

Naturally one would expect that the price of graphite would be following a similar path as lithium, which was the second best-performing commodity in 2022, and despite coming off its recent highs, lithium is still triple its three-year average. However, it appears graphite is not following suit, despite all the table pounding about the growing supply/demand imbalance, at least not yet. Although there is a slight caveat to this comment as there are no standardized prices for natural graphite and there are no fungible spot or futures markets.

Flake Graphite Price – 2022

Graphite Prices

There are a couple of reasons that graphite prices haven’t taken off like lithium prices and I’ll try to provide some clarity on that. But as we go through this it will begin to appear that it’s only a matter of time before graphite sees its time to shine. Unless of course, you are a consumer of graphite, then you might want to start working on how you will explain to Elon Musk why dropping all the prices of his Tesla models might not be a great idea.

Historically, industrial uses of graphite have always been the main driver of demand. Currently, steelmaking is still the largest source of demand for graphite, but another interesting use, at least in the U.S., is over 7% of annual demand in 2021 came from brake linings. Graphite production for these well-established industrial uses has helped keep the market well supplied, reducing price volatility. In fact, weakness in steelmaking demand, along with a return to more normal graphite production post-COVID (remember that China didn’t open up their economy until well after the rest of the world) is the primary reason for graphite prices to have come off the boil.

Synthetic Graphite

The second reason graphite prices haven’t taken off (yet) has to do with the fact that anode manufacturers have an alternative, a synthetic graphite derived from petroleum coke (a carbon-rich, solid material that comes from oil refining). I could talk for hours about petcoke from my previous career but I think that would only be interesting to me and maybe one other person I know. As noted earlier, there are a lot of opaque corners in the world of graphite, but I was able to find the following comment: “Today, synthetic graphite anodes dominate in terms of market share, accounting for approximately 57 percent of the anode market” which is attributed to Benchmark Mineral Intelligence but it might be behind their paywall. I also found this quote in an article on the Benchmark Mineral website: “Synthetic graphite anode supply grew by more than 30% during 2022, and is anticipated to even surpass that in 2023, given a supply deficit developing for natural graphite feedstock.” It appears a lot of the growing anode demand for graphite is being supplied by fossil fuels and not natural graphite.

The Time for Natural Graphite

My interpretation of all this information is that it is simply a matter of when, not if, graphite prices start to rise as we have seen with lithium. The reasons are multi-faceted and thus it could make for a slow and steady rally or if all factors coalesce at one time it could become a parabolic rise.

- As anode demand becomes a more material component of overall graphite demand it removes any previous flexibility from the supply side. If steel making or any other industrial use for graphite returns to historic levels it will quickly put pressure on the rapidly growing anode component of the demand equation. The first graph above shows how just anode growth alone will impact the overall demand outlook, let alone any other industrial uses. In the grand scheme of things, I don’t see steel consumption going to zero anytime soon freeing up that graphite supply.

- The synthetic graphite derived from petroleum coke is going to be influenced by oil prices. If oil prices go back over $100/bbl that is going to have a material impact on synthetic graphite prices. Granted, oil prices could just as easily go back to the $50-$60/bbl range and partially offset the overall graphite price rise due to general demand growth, but my personal opinion is that we’ll see $100/bbl before we see $50/bbl (perhaps an article for another day).

- But the biggest impact could come from the ESG side. “The production of synthetic graphite can be four times more carbon intensive than that of natural graphite”, another interesting fact attributable to Benchmark Mineral Intelligence that I could only find in this article. Kinda makes you think we can’t see the forest for the trees when you are making decisions like this in an effort to reduce carbon emissions. If battery makers demand low carbon anode material we could see a step change in prices, literally overnight, as natural graphite becomes the only option.

It would appear now might be a very good time to be developing a natural graphite deposit outside of China.

Disclaimer: The author of this post may or may not be a shareholder of any of the companies mentioned in this column. None of the companies discussed in the above feature have paid for this content. The writer of this article/post/column/opinion is not an investment advisor, and is neither licensed to nor is making any buy or sell recommendations. For more information about this or any other company, please review their public documents to conduct your own due diligence. To access the InvestorIntel.com disclaimer and other important legal notices, click here.